| g e n u i n e i d e a s | ||||||

|

|

|

|

|

|

|

| home | art and science |

writings | biography | food | inventions | search |

| why rebalance? |

|

Feb 2011 published in Morningstar Perspectives In the pantheon of financial planning advice, few words of conventional wisdom are more sacrosanct than these:

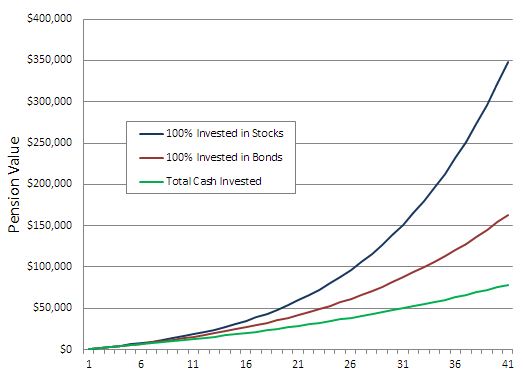

Ignore this sage advice, and your blended risk-profile might spiral out of control. Follow this advice, and you'll sail smoothly into a long retirement. Except this cornerstone of investment lore turns out to be a myth. Of course, "asset allocation" is a necessary part of any financial plan. Somehow, you must divide a new pool of cash into stocks and bonds and other assets, based on adopting one hopeful theory or another (e.g. "mid-cap stocks will rise in the recovery", or "gold is uncorrelated to real estate", and so on). Asset allocation is designed to generate a target gain with as little volatility as possible- striking a harmonious chord between risk and return. But should we rebalance those assets to maintain a fixed blend of risk and return, even when diverging gains are driving individual asset class apart? On the one hand, it seems foolish to transfer money from a hot sector to a cold, simply to maintain a fixed allocation. On the other hand, aren't you "buying low" with the hot sector's profits, thus positioning the weaker sector for greater returns in the future? Many investors systematically fiddle with their asset allocation, seeking hot sectors promising above average returns. They are not actually portfolio rebalancing so much as chasing big market swings. Real-world data indicates this strategy is rarely effective, although it has many adherents. But most people are investing as part of a long term financial plan, primarily into stocks and bonds. The penalty for not generating sufficient retirement cash flow is severe. So, around this understandable fear arose a complex infrastructure of self-help books, certified financial planners, and sophisticated investment vehicles- all designed to implement best-practices on their client's behalf. Among these practices, portfolio rebalancing is viewed as even more fundamental than asset allocation. Once the asset allocation is set, it is carved in stone for decades. Stocks are "risky", and bonds are "safe". Many investors hire professional advisors specifically to maintain, for example, a 60/40 stock/bond allocation, creating what is viewed as a worst case safety net. Even a 5% deviation from 60/40 is feared as "too risky", and immediately quashed in a spasm of asset sales and re-purchases. Many investors are willing to pay their advisors an annual 1% (or even 1.5%) fee to never step over a fixed allocation line. Except portfolio rebalancing is a mirage. Surprisingly, even large deviations around the initial target allocation delivers identical returns, at least when measured over decades of investing. And with no greater cash risk. Consider the following simple model: An investor sets aside a few percent of their salary every year, and that salary grows at the inflation rate (the details turn out to be irrelevant- in this model just remember they are investing around $1000/year into a tax efficient account). The green curve below demonstrates how that cash accumulates over a 40 year working life-- the investor put aside around $80K for retirement. But now assume they are also investing their money into either all-bonds (growing 4%/yr) or all-stocks (growing 8%/yr). Note how effectively compound interest multiplies their savings. The all-bond strategy doubled their pension fund, while the all-stock strategy delivered a remarkable 5x increase! STOCK VS BOND RETURNS

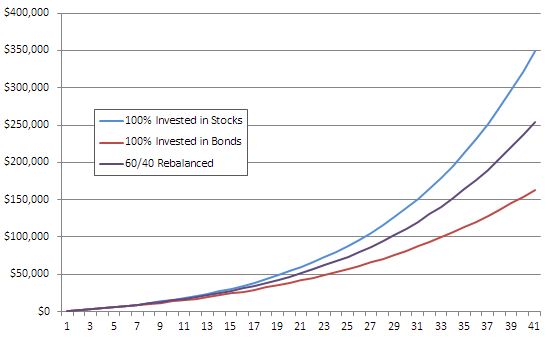

However, as the chart's title indicates, in this model both the stock and bonds markets were assumed to be calm and steady cash machines. In a calm market, only a fool invests in bonds- why ignore a perfectly safe, 2.5x greater return? Never the less, some people might still allocate their investments according to a 60/40 stock/bond rule. Just in case the stock market loses its mind- again. As you can see below, a 60/40 allocation splits the gain evenly between either extreme (which is one reason a 60/40 ratio is frequently recommended as a sober "middle" course).

60/40 ALLOCATION RETURNS GENERATED IN A "CALM" MARKET

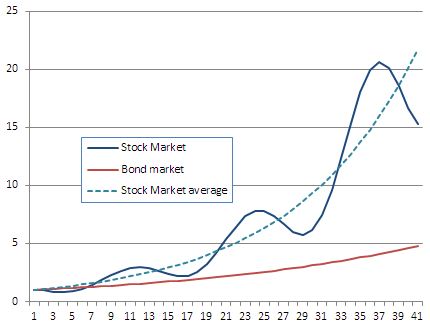

But in the real world, the stock market is rarely calm, instead fluctuating wildly compared to the relatively stable and predictable bond market. An all-stock portfolio seems too "risky" every day, not merely on the one afternoon when a black swan swims by. So how would a blended portfolio perform in a more realistic market? NORMALIZED STOCK AND BOND MARKETS

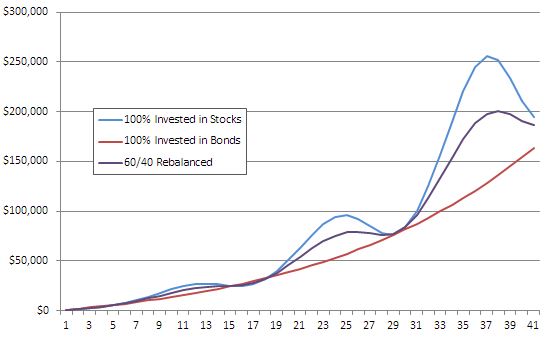

Here, I've added a periodic reversal around the mean- roughly as deep and as frequent as experienced by the actual US stock market over the last century. Bonds are assumed to remain stable throughout. This is a WORST CASE model. The investor began employment just as the market was dropping, actually losing money in the first 7 years. And, in every other decade, stock market swings erased all of the gains from contributions during that previous decade, occasionally suppressing aggregate stock returns to as low as bond returns (see the next plot, which incorporates the averaging effect of annual contributions). So, in the face of this more realistic (but worst case) model, the investor implements an annual rebalancing plan to optimize their risk/return ratio. In this worst case model during the first few years of investing they lose money (even with rebalancing) and fall behind a mere passbook savings account. Yet, despite the vicissitudes of a roiling market, compound interest eventually wins out. And, as expected, rebalancing tamps down the wilder market swings:

60/40 YEARLY REBALANCING

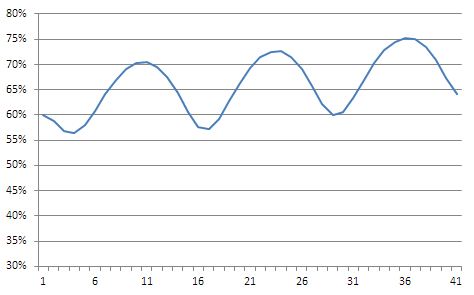

On the other hand, what would happen if you didn't rebalance at all? In other words, simply allocated your yearly $1000 contribution in a 60/40 split, but then let the portfolio allocation ride the waves of a churning financial sea. A buy and hold strategy, keeping trading costs and complexity to a minimum. Because stocks will gain (on average) more than bonds, the relative percentage of stocks vs. bonds will grow over time- as this curve demonstrates. STOCK ALLOCATION

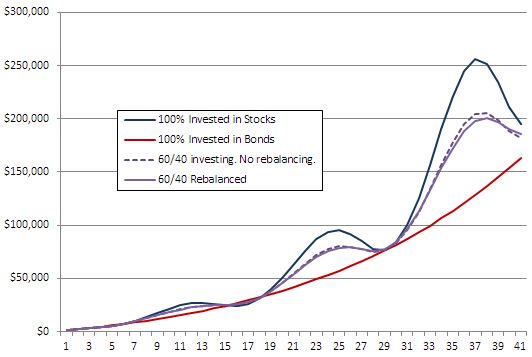

But here is the surprise- the RETURN with no rebalancing is nearly identical to the return with annual rebalancing! This conclusion is true in all cases I've analyzed, including the worse case model and different contribution schedules. I completely appreciate that without rebalancing you end up owning a greater percentage of stocks than bonds, and they might drop in value. Which seems risky. But they also GAINED more overtime, wiping out this perceived risk in absolute dollar terms. Plus you might get lucky, retiring when the market is up.

60/40 ANNUAL REBALANCING

And, there are significant rebalancing costs measured in higher trading expenses, short-term capital gains, and perhaps advisory fees. In a world where the average pension fund delivers a 6% blended return, a 1% shrinkage from higher fees would drop the value of your 40 year portfolio by around a third- more than the deepest market decline you hoped to avoid by rebalancing in the first place. A pyrrhic victory at best. While rebalancing is worshiped as a law of nature by the overwhelming majority of investors and advisors, a few commentators and academics have seen though this myth, such as Rick Ferri. In fact, not only is rebalancing unnecessary, but providing you invest over a 30 year or longer time frame, there is very little value allocating a large part of your portfolio to bonds. Look at the above chart- the return from all-stocks exceeds that of any blended strategy, except in the first 20 years, where at most you might have to wait out a small loss. A similar conclusion can be inferred from this detailed analysis of the stock market by Ed Easterling- after 25 years you achieve the average stock market return1, whether starting in the midst of the great depression or during the stagflation of the 1970s. So why does this myth persist? I believe there are three reasons- one psychological, one innumerate, and one a misapplication of the "insurance" value of bonds. On the psychological side of the ledger, its well established that people abhor losses more than they value gains. So its natural to prefer an unequivocal sure thing in bonds, over a higher value but potentially lossier allocation to stocks. In addition, people tend to discount the future over the present. So we do not trust the market to revert to average, and instead horde Krugerrands and prepare for a day when"they" destroy everything "we" have strived for. The future can be a scary place. While the numbers do not support hedging one's bet, most people sleep better at night under a blanket of false assumptions. So they rebalance. Religiously. On the mathematical side of the ledger, compound interest (and compounded losses due to higher expenses) are vastly under appreciated. The average person cannot calculate the effect of exponential growth on their savings, and thus waits too long to begin an IRA. They do not believe in regression to the mean. They worry too much about a 30% drop in their pension at age 65, but forget that 40 years of stock market investing will generate a 500% increase- plenty of room to absorb a 30% loss. The market may be irrational, but simple math is irrefutable. Yet here's the rub- we are always discussing "averages" in this analysis. If, just once-in-a-hundred times, circumstances conspires against the stock market and you would have been better off holding a higher percentage of bonds, shouldn't you take out this "insurance"? After all, its your life savings we are talking about. And here there is no unequivocal answer. The market might drop and stay down for an unusually long period of time. Can't be sure. Certainly, PE ratios are likely to fall more in line with GDP growth, and lower stock returns reduce the advantage of holding stocks over bonds. Especially if stock volatility remains high as the return gap shrinks. On the other hand, if the stock market catches the black plague, the bond market will at least catch the flu. There are no safe havens in a doomsday scenario- there is no predicting which assets will be protected by law, and which will be left high and dry. So what is my best advice? Well, I believe any significant stock market loss will be erased, given enough time. The stock market is too large to fail. It remains a surrogate for the economic strength of our nation, and the nation is fundamentally sound. My version of "insurance" is to hold, though a combination of a small pension, social security and even a few bonds, enough cash flow to live on adequately while the market is depressed. No fancy vacations, and fewer discretionary expenses while the market is down. My lifestyle becomes the buffer, not my stock holdings. In this case, keeping around 80% in stock closes the gap, and I don't care if the ratio bobs around. At the end of 40 years, and continuing into retirement, you will have more money in the bank with stocks than bonds. Even on the worse trading day of the last hundred years. That's a risk I can live with.

-------------------------------- 1 I do not mean to imply that either Easterling of Crestmont Research or Ferri of Portfolio Solutions would endorse this article's full conclusion, as they advocate slightly greater portfolio activism on behalf of their clients. They also suggest that, in some decades with an appropriate strategy, rebalancing yields fractionally higher gains than simple buy and hold. Unfortunately, such gains will not reoccur in subsequent decade if you followed the identical strategy. If you have to match the strategy to the decade, you are market timing, not rebalancing. |

Contact Greg Blonder by email here - Modified Genuine Ideas, LLC. |